The Drayage Dispatch: May 26 – Jun 1

Your weekly briefing on ports, rates, and what matters for drayage carriers.

LA/LGB Port Volume: Elevated and Holding Steady

The twin ports of Los Angeles and Long Beach closed out May with import volume running approximately 12–15% above the same week in 2025. TEU counts at the Ports of LA and LGB for the week ending June 1 came in near 185,000 combined — a level we have not seen sustained this early in the summer season in several years. The driver is familiar: importers continue front-loading inventory ahead of tariff uncertainty, and the window many shippers hoped would normalize by mid-year has stayed open longer than expected.

For drayage carriers, the implication is straightforward. Freight is moving — but so is demand on your drivers, chassis, and appointment slots. High-volume weeks like this are where margin discipline pays off or falls apart. If you are not pricing the incremental complexity of congested terminals into your rates, you are eating that cost quietly.

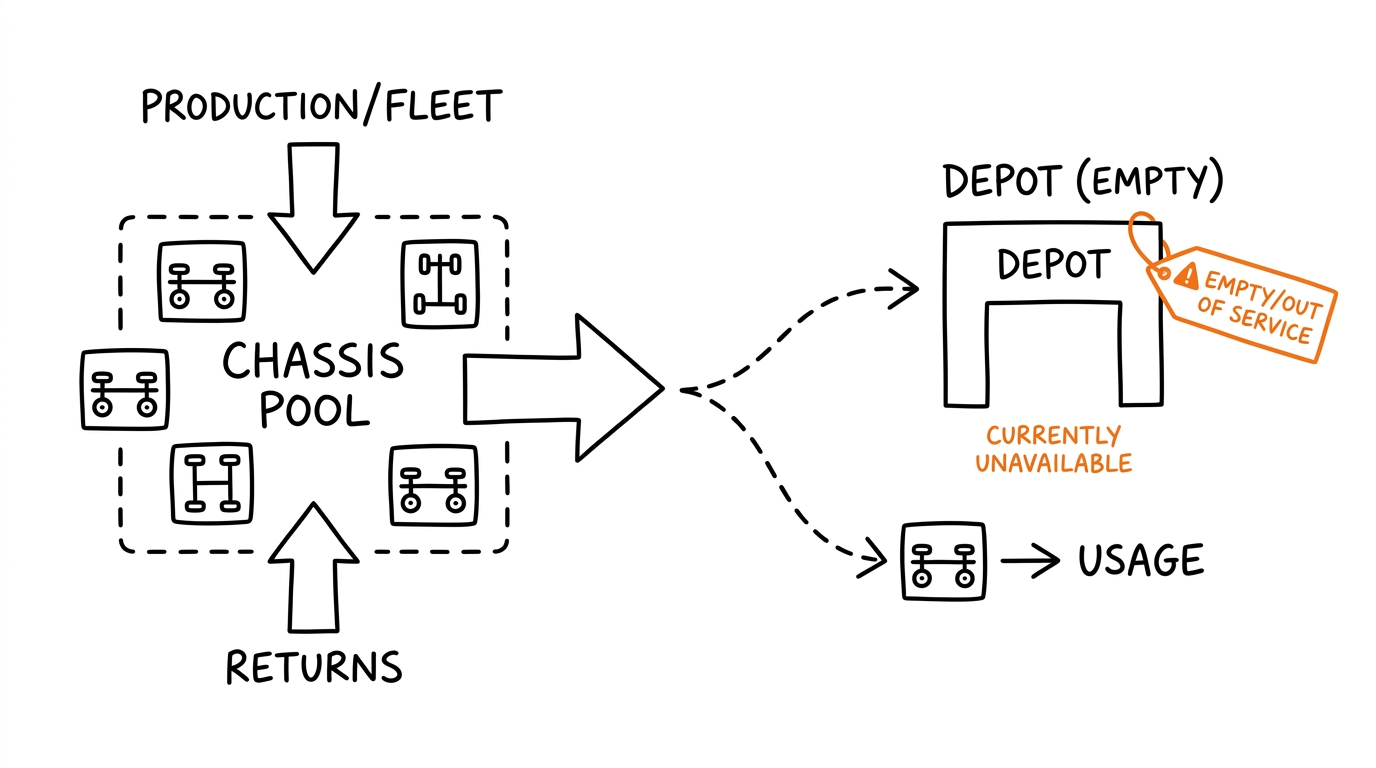

Chassis Availability: Tighter Than the Numbers Suggest

The headline chassis pool numbers at LA/LGB look passable on paper — utilization rates from the Pacific Southwest Intermodal Management (PSWIM) pool are hovering around 88–91% — but talk to any dispatcher and you will hear a different story. Splits are increasingly common. Carriers running into Fenix, TRAPAC, and ITS terminals in particular are reporting chassis split fees being triggered on a significant share of moves. At $35–$60 per split, that is a real cost hitting jobs that were quoted without that buffer.

Chassis repositioning also continues to be a friction point. Empties are accumulating in certain depot zones while other areas run dry. If you are dispatching through the San Pedro Bay complex, build in at least a $50–$75 chassis buffer on any lane where you do not have high confidence on availability.

PierPass: No New Announcements, but OffPeak Traffic Trends Worth Watching

No major PierPass fee changes were announced this week, but traffic patterns are worth monitoring. OffPeak program utilization ticked upward for the second consecutive week, with a notable increase in night gate appointments at Long Beach Container Terminal (LBCT) and Yusen Terminals. This is a positive signal: it suggests terminals are incentivizing volume distribution and some BCOs are responding.

For carriers, this creates a real opportunity. If you can optimize driver schedules around OffPeak gates, you can avoid the worst congestion windows and — depending on your customer agreements — pass through the PierPass fee savings or improve turn times enough to get more moves per driver per day.

Rate Movements: Incremental Pressure Upward

Spot drayage rates at LA/LGB continued a modest upward trend this week, driven by volume and the chassis situation described above. Short-haul lanes (0–30 miles from port) are seeing asking rates 5–8% above where they settled at the start of Q2. Inland moves in the 51–100 mile band are under less pressure — demand is there, but supply has held better.

Carriers with RFQ contracts signed in Q1 or early Q2 at flat rates may be feeling the squeeze as accessorial costs accumulate. If your contracts do not include chassis split and detention escalators, this is the week to pull out the language and review it.

Port Optimizer Data Tidbit: Dwell Times Creeping Up

According to publicly available Port Optimizer data, average container dwell times at LA/LGB terminals for the week ending June 1 came in around 4.2 days — up from 3.6 days two weeks prior. That is a meaningful increase and a leading indicator of throughput pressure. Longer dwell generally means more chassis tie-up, tighter appointment windows, and slower driver turn times.

If your average turn time has stretched past 90 minutes at any terminal this week, you are not imagining it. Factor that in when you are accepting next-day bookings or committing to volume with shippers who expect two-a-day drivers.

What to Watch: Week of June 2–8

1. MEI (Marine Exchange of Southern California) vessel queue. If anchorage counts rise above 15–20 vessels waiting to berth, expect terminal congestion to worsen by mid-week.

2. Chassis depot restocking. Several depots across Carson and Wilmington were scheduled for chassis redeliveries this weekend. Monitor whether that relieves split frequency over the coming days.

3. Diesel prices. National average diesel closed the week near $3.82/gallon. Any movement above $3.90 will trigger fuel surcharge adjustments for carriers on DOE-indexed formulas — communicate proactively with your customers if that applies to you.

4. Congressional trade hearing. A scheduled Senate Finance Committee session on tariff structure could produce signals on whether the current import surge is likely to extend or taper. No carrier should make major capacity commitments based on a single hearing, but it is worth tracking the headlines.

Forwarding this to a colleague who should be reading it? Send them to Dray Insight and tell them to subscribe. It is free.

Have a data point, terminal update, or rate movement worth sharing? Reply and we will consider it for next week's Dispatch.